05/2023 - It Never Stops

Full written article below.

Global instability and dollar decentralization continue to dominate the headlines.

The war in Ukraine continues as what appears to be a proxy war between Russia and the West. A potential aggression from China against Taiwan. Iran continuing its nuclear program, it’s unlikely Israel will simply sit back and watch this happen.

Last month we had a bank failure with Silicon Valley Bank (more reading here). Credit Suisse failed as a bank. The American economy as well as other international economies continue to load up on debt faster than the economies are growing.

Our current inflation level is still far above any acceptable level, albeit receding. The Federal Reserve has increased interest rates at the fastest pace on record.

And…. This is really just the past year. I’m sure there will be more apocalyptic headlines as we head into the summer. Then, don’t forget that we’ll be close to the election season and is likely to be bitterly partisan.

I don’t believe the bad news will stop and I really don’t think the news media outlets want the bad news to stop.

So what is an American investor to do? Unless you truly feel the world is going to end, my encouragement and continued argument is to keep investing and keep sticking to your long-term plan. The way I see it, it’s only rational.

Let me continue this point. If a rational business fails to make a profit, what do you think they’ll do? Do you think they’ll keep losing money endlessly and eventually go out of business or do you think they’ll change their tactics in order to make a profit? A rational business will work to make a profit.

A rational company, just like an individual managing their household budget, will make adjustments along the way. So when inflation is creating higher input costs to manufacture a product, companies are looking for ways to cut costs and/or increase the price of the product to preserve profitability. This really isn’t any different than what we all do when managing our expenses and income.

This is one of the benefits of a diversified portfolio of some of the largest companies in the world. Another good example is if you look at the S&P 500, this index is going to continue to shift and change as companies shift and change, as a reminder, this is a market cap weighted index. The most recent example I can think of is Silicon Valley Bank being kicked out of the S&P 500 index and being replaced with another company, Insulet. The S&P 500 is made up of close to 500 public companies who are all seeking to return a profit for their shareholders.

Using history as a guide, which has included a seemingly un-ending amount of “bad news” and multiple market declines in excess of 20%, about once a year (Capital Group), data below, the broader market has consistently marched higher.

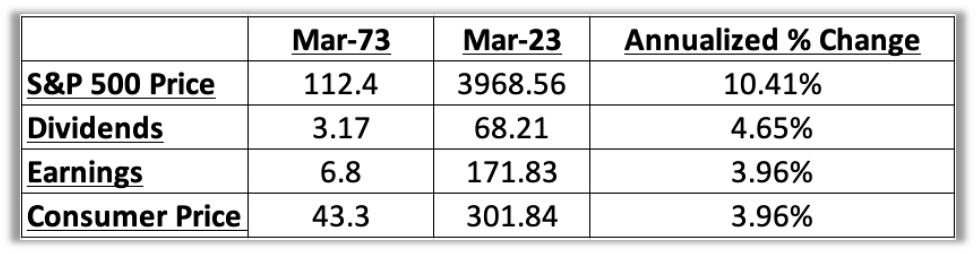

Looking specifically at the last 50 years, I can’t help but remind people that over this time period, there have been three market declines of about 50%. But even given this reality, the average market return, with dividends reinvested is still over 10% (S&P 500 data).

Let me repeat this reality, over the past 50 years, the market has dropped by about 50% three times and has regular declines of 20%, yet the long-term return is still close to +10%!

This is especially powerful when looking at inflation over this same time period, 3.96%.

Do the simple math and subtract the 10.41% S&P 500 return from inflation of 3.96% I’m still netting out a positive, or real return of 6.45%.

Yes, I can hear people saying, well sure, but don’t forget about the volatility of the S&P 500, it could be up one day and down the next. If you’re thinking this, you are 100% correct. This is precisely why the time horizon needs to be long enough to ride out the inherent volatility.

But now I can hear people saying, but what about bonds? Yes, bonds do have their spot, they do have a historical return of 5.3% (bond returns). But keep in mind that inflation has the same impact on bonds as it does stocks, so the real return is actually closer to 1-2%.

I do realize I’m getting long in the tooth, so let me summarize this quickly. Unless you think the world is going to end, I believe the only rational place to invest the majority of your long-term money is in equities, ones similarly found in the S&P 500. And as Charlie Munger stated “if you’re going to be in this game for the long pull, which is the way to do it, you better be able to handle a 50% decline without fussing too much about it.” Munger Quote

Additional Data: Each month I get asked by clients what additional resources I’m looking at. Please hear me in stating I’m not trying to predict anything whatsoever, just some of the interesting data I’m watching. This month’s list of additional data points is really just an update from some of the prior months. I’m looking for continued trends, which at least currently, are continuing.

- Did We Just Hit Bottom? – Was my blog post from Nov 2022, where I make the argument that we may have hit bottom, who knows if I’m right or wrong, it’ll take another 12-18 months to know for sure. Regardless, since the date cited, the markets are up close to 17% (dates from 10/13/22 to 04/19/23 source: Yahoo Finance)

2. BLS.gov – (above chart) showing PPI 12 month percent change, notice the sharp decline, peak was in March 2022.

3. M2 Growth vs Inflation – This is something I’ve been commenting on for close to a year and a half. Yes, I’ve been in the camp that inflation is tied to M2. We won’t know if I’m right or wrong for another year or so, but I sure like what I keep seeing. Longtermtreands.net – The trend is continuing, lower M2 (black line) is now quite a bit lower and negative along with lower inflation (red line). The next M2 update occurs on 4/25/2023.

4. Breakeven Inflation Rate - Federal Reserve – 5-Year Breakeven inflation rate is now 2.33%. When you study this chart, you’ll see it goes back to 2004.

5. Federal Reserve Balance sheet – For months the Fed was following through on it’s statement made in May 2022 of reducing the balance sheet by 47.5 billion per month in months June-Aug 2022, then reducing the balance sheet by 95 billion per month. But, just in the past month, you’ll see the balance sheet spike up by 300 billion with the new bank lending program.

Market Truths

1. The Stock Market cannot be consistently known or timed

2. The Economy (as you define it) cannot be consistently known or timed

3. Over the past 100 years, the market has returned 10.45% (with dividends reinvested). It’d be difficult for someone to achieve this return if they did not simply stay invested. Data Source

4. The average intra-year market decline is about 14% and the market drops 15% or more every 3 years. J.P. Morgan | American Funds

5. Investing in equities has historically been volatile, my guess is it always will be, however when you consider equities (using the S&P 500 as a proxy), Real Estate, short-term bonds and corporate bonds, over the long-term, equities continue to be the historical winner. To crystallize this point, just look for yourself NYU.edu.

Market Beliefs

1. Because the future cannot be known, we must embrace the belief that the world isn’t going to end during our lifetimes, and if it does, our money doesn’t matter

2. The world has continued to advance, since well before Jesus walked the earth, so assuming the world doesn’t end, it’s rational to believe the world will continue to advance

In closing: We of course cannot control what the market does from here and we cannot predict when the next market downturn will occur. But we can control our behavior to these outside events and continue to stick with our long-term investment strategy.

As always, thank you for your trust, if you have any questions/concerns please contact me.

David Hobbs, CFP®

Wealth Advisor | Owner

Hobbs Wealth Management

Standard & Poor’s 500 (S&P 500) - a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy.

Russell 2000 – The index measures the performance of the small-cap segment of the US equity universe. It is a subset of the Russell 3000 and includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

MSCI ACWI ex USA – The index measures the performance of the large and mid-cap segments of the particular regions, excluding USA equity securities, including developed and emerging market. It is free float-adjusted market-capitalization weighted.

Federal Funds Rate - refers to the target interest rate set by the Federal Open Market Committee (FOMC). This target is the rate at which commercial banks borrow and lend their excess reserves to each other overnight.

This report was prepared by Hobbs Wealth Management a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Neither the information nor any opinion expressed it so be construed as solicitation to buy or sell a security of personalized investment, tax, or legal advice. For more information please visit: https://adviserinfo.sec.gov/ and search for our firm name.

This newsletter is prepared to provide a degree of insight into the analysis used by Hobbs Wealth Management to make investment decisions. It is not a complete description of all factors used by Hobbs Wealth Management to make decisions on behalf of clients. The opinions included are not intended to be taken as fact, but are Hobbs Wealth Management’s interpretation of the impact of external events on investments.

The information herein was obtained from various sources. Hobbs Wealth Management does not guarantee the accuracy or completeness of information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. Hobbs Wealth Management assumes no obligation to update this information, or to advise on further developments relating to it.

This article contains external links directing you to a third-party website. Although we have reviewed the website prior to creating the link, we are not responsible for the content of the sites.

An index is an unmanaged portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.

The mention of specific securities and sectors illustrates the application of our investment approach only and is not to be considered a recommendation. The specific securities identified and described herein do not represent all of the securities purchased or sold for the portfolio, and it should not be assumed that investment in these securities were or will be profitable. There is no assurance that the securities purchased remain in the portfolio or that securities sold have not been repurchased. For a complete list of holdings please contact your portfolio advisor.